When looking to generate appreciable returns and increase diversification, it is natural to consider investing in foreign instruments. Currency risk then comes up, since the returns coming from these funds, stocks, bonds… need to be translated into your home currency.

The most straightforward solution to deal with this undesired extra risk is to hedge. In this context, the main objective of currency hedging is to provide the equivalent of local returns to these other foreign investors.

Hedging consists of holding the opposite currency position so that spot movements will be offset. It enables overseas stakeholders to target a return closer to the local one. But… why only closer? Shouldn’t both returns be exactly the same?

Asset Value Uncertainty

Try to imagine a utopian world where there are no lags, no frictions, no fees, and even no interest rate differentials. Well, even if they lived in this world, both returns wouldn’t be the same. The reason is quite simple: You cannot hedge a risk that you do not know you have. This idea lies in the concept I want to introduce in this post, the Asset Value Uncertainty.

It is possible to hedge the underlying value at the inception of a period, but it is impossible to hedge the currency risk that arises from the variation of its value, merely because it was unknown at the time of hedging. This means that by the end of the period, the currency exposure will be either under or over-hedged, depending on gains or losses that the value experimented with, respectively.

Going back to the post An intuition behind currency risk, Asset Value Uncertainty corresponds to the last term of the equation:

[latex] R=(1+r_s)(1+r_e)-1=r_s+r_e+r_s*r_e [/latex]

Thus, the realized impact of Asset Value Uncertainty can be either positive or negative, depending on both the underlying asset return ([latex]r_e[/latex]) and the spot return ([latex]r_s[/latex]). It is supposed to be insignificant, but, once you have decided to mitigate currency risk, it may gain importance.

Checking some numbers

Let’s try with some numbers to check how negligible Asset Value Uncertainty actually is.

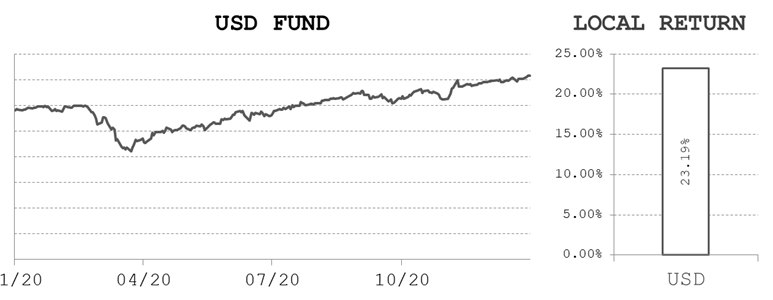

Local return

Let’s focus our attention on a USD-denominated fund chosen at random. Imagine a US stakeholder selected this fund as part of her portfolio. Her result during the past year was the following, corresponding exactly to the fund result:

Now, I have created some diverse international investors, in particular: CAD, GBP, JPY, AUD, EUR & CHF. All of them need to translate the previous fund result back into their home currencies. First, we suppose that they accepted currency risk, keeping their investment unhedged during the whole of 2020:

Currency risk damaged all the exemplified unhedged results. It would have been better not to be exposed to the USD movement risk, i. e., to have been hedged during this period.

Hedged return

Now, let’s simulate “perfect” hedging in an unrealistic world without any lags, frictions, fees,… We also assume a world where interest rates are the same for all the studied currencies, so swap points on the forward contracts are exactly zero. With these conditions, the only divergence between the local stakeholder and those perfectly hedged is the Asset Value Uncertainty, i.e. the spot effect over the gain of the fund that wasn’t hedged at the beginning of the year. As we can see it is quite small but not negligible; it reaches just over -2% in the worst case:

Inside Asset Value Uncertainty

The Asset Value Uncertainty impact was negative for all these international results. Is this normally the case? No, not necessarily.

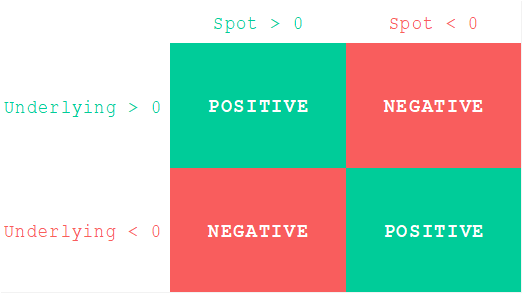

As the first figure shows, Asset Value Uncertainty corresponds to the composition of the underlying and spot returns. USD depreciated against CAD, GBP, JPY, AUD, EUR, and CHF during 2020, therefore any successful foreign participations were negatively altered by this Asset Value Uncertainty. Currency risk was against the USD positions and, even though you would hedge this negative effect, some damage remains as you couldn’t have hedged the annual return of your investment, which was positive.

As you can imagine, if the USD had appreciated, then Asset Value Uncertainty would impact positively. This is the case for BRL, PEN, MXN, ZAR, INR, and THB investors, because USD appreciated against their respective home currencies in 2020. A different example of positive Asset Value Uncertainty is those noticed by the first set of investors if they would have taken part in an unsuccessful USD fund, with a negative return. The following figure contains the whole picture regarding the sign of the combination (underlying, spot):

To sum up

In a hedging context, Asset Value Uncertainty is an unavoidable currency risk coming from the unpredictable performance of your foreign investment. It’s small in comparison to the absolute currency movement, but when currency risk has been hedged, then it could turn into a significant effect.

References

Share Class Hedging: Performance Attribution – Jordan Alexiev, Jay Moore, David Turkington